|

Comparisons with Onshore Wind Power Industry in Denmark

What comparisons can be drawn from the development of the Danish on-shore wind industry from the 1970’s?

- UK & Scotland is in a similar situation to Denmark in the 1970’s

- Scotland is ideally placed to mimic the Dane’s success story

- Many of the World’s leading academics and experts in wave and tidal energy are in resident in the UK

- Aside from the energy issue there is a considerable potential to export technology worldwide and become a World leader in MCT’s

- Benefits to export economy and skilled jobs market

In depth Analysis

Evolution of Danish Wind Power Industry

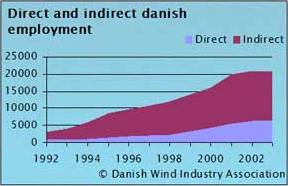

Workforce in 1981 was only a few hundred

- Now total employment has expanded to 20,000

Note

Calculation methods in WindPowerNote No. 2, November 1995.

Employment figures are mid-year figures.

Source: http://www.windpower.org/en/stats/totalemployment.htm

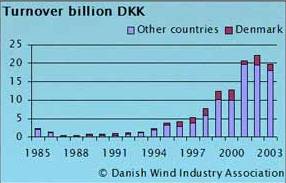

Industry now has turnover of DKK 20 billion (1.5 million Euros)

Source: http://www.windpower.org/en/stats/turnover.htm

- Export of technology

- Around 50% of installed wind capacity is Danish in origin

- 4 major turbine manufacturers:

- Vestas

- NEG Micon

- Bonus

- Nordex (no longer manufacture turbines)

- Numerous smaller component manufacturers

Why the success story?

- By accident?

- As a result of concerted effort by Danish government to promote the industry?

Danish Government Commitments

- Refusal to adopt nuclear power

- Halt to proposed new coal fired plants

- Grants for R&D

- Tariffs & incentives

- Offshore plans

- Higher wind velocities leading to greater energy yields (cubic relationship)

- Potential to produce 50% of Denmark’s electrical demand (1/4 of total energy demand)

- Grid priority to renewable-generated electricity

- Historical Commitment to expanding Wind Power Industry by Policy and continual and consistent adoption by successive governments

- 1970’s

- Mandatory purchase of electricity from private wind companies at 85% retail price

- 1979-1989

- Capital Grants programme

- “10% from wind” target set in mid 80’s

- Target met and exceeded by 2000

- 1996

- Energy 21, target of 45% from wind by 2030

- Will entail additional 5,500 MW installed capacity

- Likely to be met by offshore developments

- 2003

- Improvement of subsidies and inclusion of earlier projects in new subsidy schemes to safeguard investments

Lessons from Danish Experience

- Government must provide incentive to investors by:

- removing uncertainty and unnecessary risk

- Pledging long term tariffs and grants

- Increase value of capital grants for marine renewables projects

- Manage the £50 million “R&D to pre-commercial” fund diligently

- Promoting Connection of renewables to grid

- Resolving electricity market trading barriers

- Be technology/ source specific with ROC/ROS

- Otherwise utility companies will opt for cheapest form of renewable generation (e.g biomass, on-shore wind, hydro etc.)

Implementing Danish Lessons into a UK context

- Look at progression of UK on-shore wind industry

- Will marine renewables take a similar path?

- OR will it be more closely aligned with offshore wind or indeed offshore industry in general?

- What are the similarities and differences?

- Safety issues

- Installation costs- moorings, seabed assessment etc.

- Planning permission

- Grid connection

- More costly by a factor of 1 magnitude compared with on-shore wind

- Leading to increased capital costs from outset

- Different funding strategy required

- Economies of scale

- Larger scale farms will lead to reduced costs

- Even if government fails to attract backing from a moral “carbon-reducing” perspective, one cannot ignore the huge potential for economic growth existing in marine renewables

- Government has 2 options:

- “import” clean energy technologies

- Effectively allowing other countries to invest and carry out the work

- Or develop World’s leading marine renewables industry in the UK

- The later option would:

- Enable UK to reap the combined benefits of economic growth and diversity

- In addition to meeting the environmental and carbon sequestration challenge, so clearly sighted by the government as a target for 2020 and beyond

|

|